How Much Do You Need for a Down Payment in Montgomery County, PA? (2026 Guide)

If you’re planning to buy a home in Montgomery County, PA in 2026, one of the first questions you’ll ask is:

“How much do I really need for a down payment?”

The truth is, many homebuyers are surprised to learn they may not need as much upfront as they once thought. Your exact down payment depends on several factors — including loan type, purchase price, credit score, and whether you qualify for local or state assistance programs.

The 20% Down Payment Myth

You don’t need 20% down to buy a home in Montgomery County. While putting 20% down helps you avoid private mortgage insurance (PMI), that’s not the only path to homeownership.

Today’s most common loan programs offer options such as:

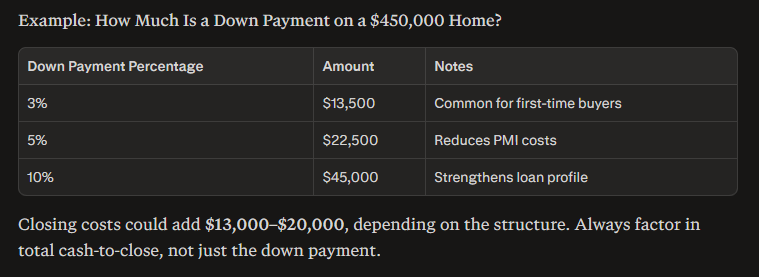

3% down (Conventional loans for qualified buyers)

3.5% down (FHA loans with federal backing)

5% down (Common for repeat buyers)

0% down (VA loans for eligible veterans and active-duty service members)

Each option has its pros and cons, so it’s important to align your choice with your financial comfort and long-term goals.

Common Loan Options for Montgomery County Homebuyers

Conventional Loans

Minimum down payment: ~3% for first-time buyers

PMI required until you reach 20% equity

Typically stronger for buyers with good credit

FHA Loans

Minimum down payment: 3.5%

More flexible credit guidelines

Includes upfront and annual mortgage insurance

VA Loans

Available to eligible veterans and service members

May offer 0% down payment

Competitive interest rates and no PMI

Down Payment Assistance & First-Time Buyer Programs

If you’re a first-time homebuyer in Montgomery County, you may qualify for state and local assistance. Programs in Pennsylvania often provide:

Down payment and closing cost grants

Forgivable loans or deferred-payment options

Reduced interest rates through PHFA (Pennsylvania Housing Finance Agency)

Eligibility is typically based on income, location, and home price. Your lender or real estate professional can help determine which programs you qualify for.

What to Budget Beyond the Down Payment

A down payment isn’t the only upfront cost when buying a house. Be sure to account for:

Closing costs (typically 3–5% of the purchase price)

Title and lender fees

Escrow deposits (taxes and insurance)

Home inspection and appraisal fees

In Montgomery County, these costs can add several thousand dollars depending on your loan type and property price.

Should You Put More Down?

Putting more money down can:

Lower your monthly mortgage payment

Reduce or eliminate PMI

Strengthen your offer in competitive markets

However, it’s just as important to keep an emergency fund and maintain liquidity. The right balance depends on your income stability, comfort level, and long-term plans.

Strategy: Down Payment vs. Monthly Payment

Every buyer has different priorities:

Lower down payment, higher monthly: Keeps more cash available for home improvements or savings.

Higher down payment, lower monthly: Reduces overall loan costs and boosts offer competitiveness.

Talking through your options with a local lender will help tailor your approach.

How Montgomery County Property Taxes Affect Affordability

Don’t forget that property taxes vary widely across the county. Before finalizing your down payment and loan strategy, factor in:

Township tax rates (e.g., Lower Merion vs. Pottstown differ noticeably)

School district assessments

HOA or condo fees if applicable

Your total monthly cost = Mortgage + Taxes + Insurance + HOA (if any). Keeping this full number in view helps you stay comfortably within budget.

Want to Know Exactly How Much You’ll Need?

Let’s personalize your numbers. We’ll review:

Your income and credit profile

Target purchase price range

Loan and assistance program options

Estimated down payment and monthly costs

👉 Schedule Your Buyer Strategy Consultation

Together, we’ll map out a clear budget and position you to buy confidently in today’s market.

FAQs About Down Payments in Montgomery County

Do I need 20% down to buy a home?

No. Most buyers in 2026 put down between 3% and 10%.

Can I buy with 3% down?

Yes, if you meet loan and credit requirements.

Are there grants or assistance programs in Montgomery County?

Yes — many PA buyers use programs through PHFA or local municipalities.

Does a larger down payment make my offer stronger?

In many cases, yes — it signals financial stability and can appeal to sellers.

Ready to Move From Planning to Buying?

The right down payment strategy paves the way to homeownership success.

Let’s figure out your best path today.