FHA vs Conventional Loans: Which Is Better for First-Time Buyers in Pennsylvania? (2026 Guide)

If you’re buying your first home in Montgomery County, Philadelphia, Bucks County, or the surrounding suburbs, one of your biggest decisions is FHA vs Conventional. Both loan types can work well for first-time buyers in Pennsylvania, but the better fit depends on your credit score, savings, debt, and how competitive your target neighborhood is.

I’m Shaina McAndrews, team leader at eXp Realty and founder of MontCoLiving. My job is not just to help you get approved — it’s to help you choose the financing strategy that strengthens your offer today and supports your long-term wealth.

What Is an FHA Loan?

FHA loans are mortgages insured by the Federal Housing Administration and are popular with first-time buyers because of their flexible credit and down payment requirements.

FHA Basics (Pennsylvania)

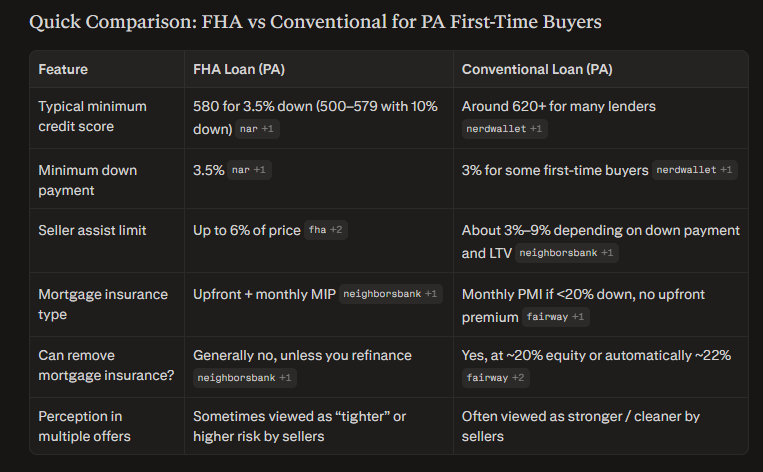

Minimum credit score: typically 580 for 3.5% down; 500–579 may qualify with 10% down

Minimum down payment: 3.5% with 580+ credit score

Seller assist allowed: up to 6% of the purchase price toward buyer costs

Mortgage insurance: required upfront and monthly (MIP), often for the life of the loan with <10% down

FHA loans are often helpful for buyers who:

Have limited savings for down payment

Have credit scores below 680

Need higher seller assist to help cover closing costs

Are rebuilding credit after past issues

The trade-off is that FHA mortgage insurance can be more expensive and longer-lasting, especially if you put less than 10% down.

What Is a Conventional Loan?

Conventional loans are not government-insured; they follow Fannie Mae and Freddie Mac guidelines and are typically viewed as stronger financing in multiple-offer situations.

Conventional Basics (Pennsylvania)

Minimum credit score: often 620+ for many lenders

Minimum down payment: as low as 3% for qualifying first-time buyers

Seller assist allowed: typically 3% of the price with low down payments, up to 6–9% with higher down payments

Mortgage insurance (PMI): required under 20% down, but can be removed once you reach about 20% equity

Conventional loans are often better for buyers who:

Have 680+ credit scores

Have stable income and lower debt

Want PMI that can be removed in the future

Are competing in multiple-offer situations where sellers prefer conventional financing

Which Loan Is Stronger in a Competitive Pennsylvania Market?

In hot areas like:

Ambler

Blue Bell

Lower Gwynedd

King of Prussia

Manayunk

Fishtown

Sellers and listing agents often perceive conventional loans as stronger than FHA, even if the monthly payment difference for you isn’t huge.

Why conventional can be viewed as stronger:

FHA appraisals may apply stricter property condition standards, and sellers worry about repair requirements or delays.

Some sellers assume conventional borrowers are more financially solid (even though that isn’t always true).

This doesn’t make FHA a “bad loan” — it just means your loan choice becomes part of your negotiation strategy, especially in multiple-offer situations.

How Mortgage Insurance Differs (Long-Term Cost)

FHA Mortgage Insurance (MIP)

Upfront mortgage insurance premium (usually financed into the loan)

Monthly MIP added to your payment

For most FHA loans with <10% down, MIP typically remains for the life of the loan unless you refinance into another product later

Conventional Private Mortgage Insurance (PMI)

No FHA-style upfront MIP in most cases

Monthly PMI is required with less than 20% down, but:

You can usually request removal at 20% equity based on your loan-to-value.

Lenders often automatically remove PMI at 22% equity.

For buyers planning to stay in their home long-term and who qualify credit-wise, conventional loans often become more cost-effective over time because PMI eventually goes away.

When FHA May Be the Better Choice

FHA can be the better option for a first-time buyer in Pennsylvania if:

Your credit score is roughly 580–660 and you want a competitive rate

You need more seller assist to cover closing costs (up to 6% allowed)

Your debt-to-income ratio is higher and conventional underwriting is tighter

You’re purchasing at a lower price point or in an area where FHA is commonly used

FHA can open doors when conventional underwriting would issue a denial or a weaker approval.

When Conventional May Be the Better Choice

Conventional often shines when:

Your credit score is 680+ and you qualify for better pricing

You want mortgage insurance that can be removed as you build equity

You’re shopping in highly competitive neighborhoods where sellers prefer conventional financing

You plan to keep the home and want the best long-term cost structure

Conventional loans can position you as a stronger, simpler buyer in the eyes of the seller, which can matter more than a slightly higher offer price.

Frequently Asked Questions

Is FHA better for first-time buyers in Pennsylvania?

It depends. FHA is more flexible with lower credit scores and limited savings, but long-term mortgage insurance costs are usually higher and last longer than conventional PMI.

Is a conventional loan harder to qualify for?

Generally yes. Conventional loans tend to require higher credit scores and stronger overall profiles, but they can offer better long-term cost and stronger positioning in competitive markets.

Can I switch from FHA to conventional later?

Yes. Many buyers start with an FHA loan to get into a home and later refinance into a conventional loan once credit improves and equity increases, which can remove FHA mortgage insurance.

Which loan usually wins in a multiple-offer situation?

All else equal, sellers often prefer conventional financing, but offer structure, price, appraisal protections, and timelines can matter more than loan type alone.

The Bigger Question: What Is Your Long-Term Plan?

Choosing FHA vs Conventional in PA isn’t just about getting a quick approval. We look at:

How long you plan to stay in the home

How quickly local values are appreciating

Your comfort level with the monthly payment

Whether you want flexibility to remove PMI or refinance

How your loan choice affects your offer strength in your specific target neighborhoods

Your first home should be a stepping stone, not a financial trap.

Why Work With Shaina McAndrews?

First-time buyers need more than a list of loan types — they need a strategy tailored to their numbers and market. My team:

Evaluates your financing options before we start touring homes

Coordinates with trusted local lenders who understand first-time buyer programs

Structures offers with the right loan, seller assist, and terms for each property

Protects you through inspections, appraisal, and negotiations

You deserve a clear, customized plan for buying in Montgomery County, Philadelphia, and the surrounding Pennsylvania markets.

Ready to Explore Your Loan Options?

👉 Schedule your buyer strategy consultation

👉 Curious what homes are selling for in your target neighborhood?