Online affordability calculators make it look simple, but in Montgomery County PA your real monthly payment depends heavily on local property taxes, insurance, and today’s prices. In early 2026, the typical Montgomery County home value is in the mid‑$470,000s, with a January 2026 median sale price around $450,000 and roughly 2–3% annual appreciation.

On top of your mortgage principal and interest, you’ll need to budget for county/municipal/school taxes, homeowners insurance, and things most calculators gloss over—maintenance, utilities, and closing costs. This guide breaks down real ballpark monthly numbers so you can see what’s realistic, then invites you to map your exact numbers instead of guessing.

If you want a custom affordability breakdown based on your income, debts, and target towns, you can schedule a quick consultation here: https://calendly.com/agentshainamc/quick-call

Step 1: Where Prices Are in Montgomery County PA (2026)

Before you run numbers, it helps to know what homes actually cost here right now.

Current price trends

January 2026 median sale price: about $450,000, up roughly 2.9–3.2% from January 2025.

Typical county home value: about $470,000–$475,000, with roughly 1.7–3.3% year‑over‑year appreciation.

2024 planning data: median around $457,000, up 7% from 2023; new construction medians over $660,000.

Translation: prices aren’t crashing, but they’re not spiking either—they’re moving steadily, which matters if you’re thinking of “waiting a year.”

To see Montgomery County PA homes for sale in your likely price range right now, you can search directly here: https://zenlist.com/a/shaina.mcandrews

Step 2: Key Local Cost Drivers Most Calculators Miss

Most big national calculators estimate principal and interest correctly but under‑estimate your PITI (Principal, Interest, Taxes, Insurance) and ongoing costs in a specific county.

Property taxes

Montgomery County’s county‑level tax rate was raised to 5.642 mills for 2025, a 9% increase over 2024, meaning about $5.642 per $1,000 of assessed value at the county level alone.

For an “average single‑family home” assessed around $520,100, the county CFO estimated county property taxes of about $965/year, roughly $80/month—and that’s only the county portion, not school and municipal taxes.

School district and municipal millage often add several times the county portion, so total property taxes in many Montgomery County suburbs commonly land in the 1.5–2.5% of market value per year range, depending on district and assessment.

Homeowners insurance

One 2026 analysis estimates average homeowners insurance in Pennsylvania at $1,278 per year for a policy with $300,000 in dwelling coverage (about $107/month).

Another 2025 roundup put Pennsylvania’s average closer to $1,014/year (about $85/month) for a typical HO‑3 policy, noting that premiums scale with home value.

A 2025 report also notes that Pennsylvania homeowners saw about a 44% increase in premiums between 2021 and 2024, bringing many policies to around $1,440/year, or $120/month.

For a $400K–$600K home in Montgomery County, it’s reasonable to estimate $100–$150/month for homeowners insurance, depending on coverage and specifics.

Hidden and often‑ignored costs

Maintenance and repairs (rule of thumb: 1–2% of home value per year in the long run).

Utilities (often higher than a same‑size apartment).

HOA/condo fees where applicable.

Closing costs (typically several percent of the purchase price, though often paid once, not monthly).

The point: online calculators that only show principal + interest can understate your real monthly housing cost by hundreds of dollars.

Real‑World Monthly Payment Examples (2026 Conditions)

For illustration, let’s assume:

30‑year fixed mortgage.

Interest rate in the low‑6% range (approximate current environment).

10% down payment (enough to keep numbers realistic for many buyers).

Property tax effective rate: roughly 2% of purchase price per year (ballpark for many Montco towns once county, school, and municipal taxes are combined).

Insurance: about $120/month (mid‑range Pennsylvania estimate).

These are examples, not quotes, but they give you a more honest picture than a bare calculator.

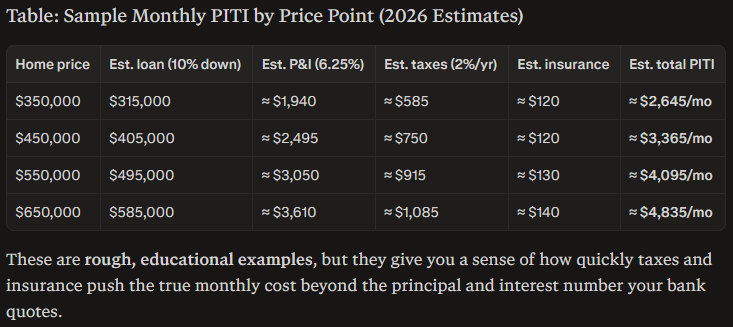

Example 1: Affording a $350,000 home

Price: $350,000

10% down: $35,000

Loan amount: $315,000

Approximate monthly:

Principal & interest (around 6.25%): ≈ $1,940/month

Taxes (2% of price = $7,000/year): ≈ $585/month

Insurance: ≈ $120/month

Estimated total monthly PITI: about $2,645/month

This might align with some starter homes or townhomes depending on the specific Montgomery County neighborhood and current list prices.

Example 2: Affording a $450,000 home (around current median)

Price: $450,000

10% down: $45,000

Loan amount: $405,000

Approximate monthly:

Principal & interest (around 6.25%): ≈ $2,495/month

Taxes (2% of price = $9,000/year): ≈ $750/month

Insurance: ≈ $120/month

Estimated total monthly PITI: about $3,365/month

This price point is close to the January 2026 median sale price, meaning it reflects a “typical” Montgomery County home in many suburbs, not a luxury outlier.

Example 3: Affording a $550,000 home

Price: $550,000

10% down: $55,000

Loan amount: $495,000

Approximate monthly:

Principal & interest (around 6.25%): ≈ $3,050/month

Taxes (2% of price = $11,000/year): ≈ $915/month

Insurance: ≈ $130/month

Estimated total monthly PITI: about $4,095/month

This band often covers larger move‑up homes, some new construction, or properties in high‑demand school districts.

Example 4: Affording a $650,000 home (higher‑end but not luxury)

Price: $650,000

10% down: $65,000

Loan amount: $585,000

Approximate monthly:

Principal & interest (around 6.25%): ≈ $3,610/month

Taxes (2% of price = $13,000/year): ≈ $1,085/month

Insurance: ≈ $140/month

Estimated total monthly PITI: about $4,835/month

This level might cover larger or newer homes in some of Montgomery County’s most sought‑after communities.

If you’d like to plug in your actual interest rate quote, down payment, and target towns, the Shaina McAndrews Team can run a personalized payment breakdown with real tax estimates: https://calendly.com/agentshainamc/quick-call

Real Affordability vs Online Calculators

Why generic calculators are often misleading

Most national calculators:

Use simplified or low property tax assumptions that don’t match Montgomery County’s mix of county, municipal, and school millage.

Under‑estimate insurance, especially after Pennsylvania’s recent premium increases.

Ignore local price dynamics (e.g., median near $450K, typical value around $470K, not $250K).

Rarely include HOA/condo fees, maintenance, and realistic closing costs.

That’s why buyers are often surprised when the bank or their agent shows them the true monthly and cash‑to‑close numbers.

What “real affordability” looks like

Real affordability means aligning:

Your comfortable monthly payment.

Your likely price range in specific Montgomery County towns.

Your cash needed for down payment, closing costs, and initial reserves.

For example, if your comfortable top‑end payment is $3,000/month, the $450K example above might be a stretch once taxes and insurance are factored in, whereas a $375K–$400K budget might be a better fit.

The goal isn’t to max out pre‑approval; it’s to match a Montgomery County PA home to a payment you can live with comfortably.

Don’t Forget: Down Payment, Closing Costs, and Cash Buffer

Down payment realities

You don’t need 20% down to buy in Montgomery County, but your down payment:

Impacts your monthly payment.

Affects whether you pay mortgage insurance (MI).

Can determine how competitive your offer looks in certain price bands.

Buyers here commonly use 3–10% down depending on their loan type and financial profile, and then plan to build equity over time rather than waiting years to hit 20% before ever buying.

Closing costs

Closing costs in Pennsylvania typically run several percent of the purchase price and can include:

Transfer tax (split between buyer and seller in many deals).

Lender fees, title insurance, and recording costs.

Prepaid taxes and insurance.

On a $450,000 home, it’s not unusual for total closing costs (including prepaids) to fall in the $15,000–$20,000 range, depending on loan structure and credits, which is in addition to your down payment.

Cash buffer after closing

A truly smart affordability plan leaves:

At least a basic emergency fund (3–6 months of expenses).

Some funds for immediate repairs or furnishings.

You don’t want to be house‑poor in a market where taxes and maintenance are real factors.

If you’d like help reverse‑engineering from “cash I have” to “home I can comfortably buy,” that’s exactly what a planning call is for: https://calendly.com/agentshainamc/quick-call

How Much House Can You Afford? A Simple Framework

Rather than starting with “What price can I afford?”, it helps to work backward from your life and monthly comfort zone.

1. Define your true monthly comfort number

Look at your net income and current rent.

Decide on a monthly payment that feels sustainable, not just “maximum you can survive.”

For many buyers, this is in a range where they can still save for retirement, travel, and future goals.

2. Layer in local taxes and insurance

Take your monthly comfort number and subtract realistic estimates for:

Taxes (use 1.8–2.3% of price per year as a ballpark in many Montgomery County suburbs, then translate to monthly).

Insurance ($100–$150/month for many standard policies in PA, higher for larger homes).

What’s left is what you can reasonably allocate to principal and interest.

3. Match P&I to a price bracket

Using your P&I allowance and current interest rate, you can target a price range that works for you in real local terms. Then, cross‑reference that with where prices actually are in towns you like.

For example:

If you can comfortably handle a $2,700/month total payment, you may be closer to the $375K–$425K range than to the full median of $450K, depending on exact taxes and rate.

If you can handle $3,500–$3,800/month, you might have room to shop closer to or above the current county median value.

This is where a quick session with a local agent and lender can turn guesswork into clear, personalized ranges.

FAQ: Affordability in Montgomery County PA

What is the average home price in Montgomery County PA in 2026?

Recent market data shows a January 2026 median sale price around $450,000, with a typical county home value in the $470,000–$475,000 range.

How high are property taxes in Montgomery County?

County property tax alone is about 5.642 mills (roughly $5.642 per $1,000 of assessed value) for 2025, and an average single‑family home valued at around $520,100 pays about $965/year in county taxes. Once you add school and municipal millage, total taxes in many areas can land around 1.5–2.5% of market value per year, depending on district and assessment.

How much does homeowners insurance cost in Pennsylvania?

State‑level estimates put average homeowners insurance around $1,014–$1,440 per year (roughly $85–$120/month), depending on coverage and home value. Higher‑value homes and broader coverage limits will increase this amount.

How much should I budget for maintenance?

A common rule of thumb is 1–2% of the home’s value per year over the long run. On a $450,000 home, that’s $4,500–$9,000/year on average, though actual expenses can vary widely year to year.

Why do your estimates look higher than online calculators?

Because they bake in Montgomery County’s real property tax environment, more realistic insurance costs, and current local prices instead of national averages. Generic calculators tend to use lower tax assumptions and ignore many local cost drivers.

How do I figure out exactly how much I can afford?

The most accurate approach is to combine:

A local lender’s pre‑approval with real rate and closing cost estimates.

Montgomery County‑specific tax and insurance assumptions.

Your personal comfort level with monthly payments and reserves.

That’s where a 15–30 minute planning call can save you months of uncertainty.

You can:

Map your exact affordability numbers with the Shaina McAndrews Team: https://calendly.com/agentshainamc/quick-call

Search Montgomery County PA homes for sale that match your budget: https://zenlist.com/a/shaina.mcandrews

Get a quick home value estimate if you’re selling and buying: http://app.cloudcma.com/api_widget/4c119a73549ddc99191fd9e9192a3990/show?post_url=https://app.cloudcma.com&source_url=ua

Roughly what total monthly payment (including taxes and insurance) feels truly comfortable for you—closer to $2,500, $3,000, $3,500, or something else?